Modernising core banking: a strategic imperative for future-proofing today’s banks

As the financial industry undergoes rapid transformation, modernising core banking systems is no longer optional - it’s a necessity. With many banks still operating on legacy systems, some of which were implemented 30 to 40 years ago, these aging platforms, often heavily customised, struggle to keep pace with the demands of digital banking, real-time transactions, and seamless integration with fintech partners.

Authors

Modernising core banking systems can drive several strategic benefits:

Customer experience: modern systems enable real-time processing and faster product releases, enhancing customer satisfaction and competitiveness.

Operational efficiency: streamlined operations and reduced manual processes can significantly lower operational costs. For example, a well-executed DevOps and release management plan can lead to a 25-30% boost in capacity creation, a 50-75% decrease in time to market, and over a 50% drop in failure rates.

Regulatory compliance: enhanced systems can more easily adapt to regulatory changes, reducing the risk of non-compliance.

Additionally, core banking transformation has been de-risked by new approaches which target specific product or business use cases for a minimum viable product, which can then be scaled to include other products or business areas and avoid a “big bang” cut over to a new platform and the associated risk of failure.

Why act now?

The urgency to modernise core banking systems stems from both immediate and long-term considerations:

Incremental value from investment: modernisation isn't just a cost; it's an investment that delivers incremental value. With many banks often using core systems from the 1980s and 1990s, banks can start seeing benefits from improved efficiency and customer satisfaction almost immediately, which can translate into increased revenue and market share.

Short-term value creation: quick wins are achievable with a modular approach. By modernising specific components incrementally, banks can improve services and reduce costs without waiting for a full system overhaul. With well-defined APIs able to advance concept to deployment of a viable product within 30 – 60 days.

Competitive pressure: with digital-native challengers and fintech companies disrupting the market, traditional banks must modernise to stay competitive. Delaying this transformation risks falling behind in offering innovative and efficient banking solutions.

Regulatory landscape: the regulatory environment is continuously evolving. Modern systems can help banks more efficiently comply with new regulations, avoiding potential fines and reputational damage.

Figure 1: External factors to consider when developing the bank of the future

Figure 2: Internal factors to consider when developing the bank of the future

Embarking on the journey, with confidence

Embarking on core banking modernisation requires strategic thinking to ensure you are modernising for future as well as current business needs. Valentia Partners, alongside a 10x, offers a comprehensive approach to ensure your bank's success.

Designing for the future

Successful modernisation starts with understanding and assessing core capabilities against that current and future business need. Valentia Partners facilitates this through:

Evaluating current state: assess product offerings, customer and account volumes, service models, transaction volumes, technology architecture, and organisational structure.

Identifying future needs: align capabilities with future product and service offerings to meet customer expectations and regulatory requirements.

Capability assessment: highlight inefficiencies, limitations and risks and assign weighting to them.

Understanding the assessment: decomposing and understanding capabilities at a people, process, technology, and data level is vital to designing the right solution and approach.

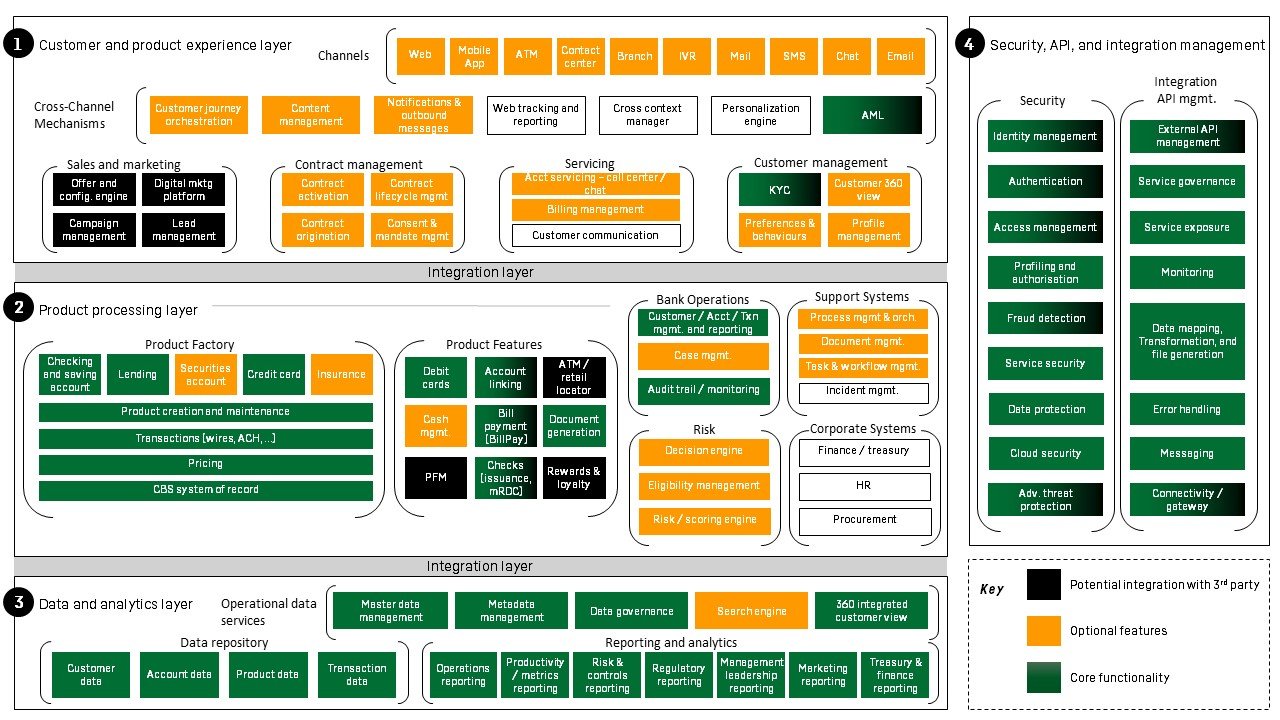

Figure 3: Identify the perimeter of core technology functionality

Setting strong foundations

Insights gained from understanding and assessing core capabilities are instrumental in developing a targeted modernisation roadmap. Valentia Partners offers a one-day workshop designed to kickstart this process. Outputs from the workshop are foundational in shaping the approach for a targeted modernisation plan, through:

Initial insights: offer a snapshot of the current state and improvement opportunities.

Stakeholder engagement: ensure alignment and buy-in.

Skeleton of a roadmap: outline modernisation pathways, prioritising initiatives based on strategic importance and impact.

This workshop provides a clear starting point, ensuring your modernisation efforts are strategically sound and aligned with your long-term goals.

Key takeaways

Core banking modernisation transforms your bank to meet future challenges. By understanding core capabilities and building a targeted roadmap, you enhance operational efficiency, improve customer satisfaction, and drive innovation. Valentia Partners' expert guidance combined with 10x Banking’s scalable, resilient, and flexible technology, ensures your bank's success in the digital era. Begin the journey today and secure your bank's future.

Related Articles